Blog

5 Ways Technology Can Help with SMCR Compliance

One of the biggest changes to FCA regulation in recent years was the need to…

How To Embrace Technology but Keep Your Humanity – Implementing A RegTech Solution

Today, the majority of our business and personal lives are dominated by our…

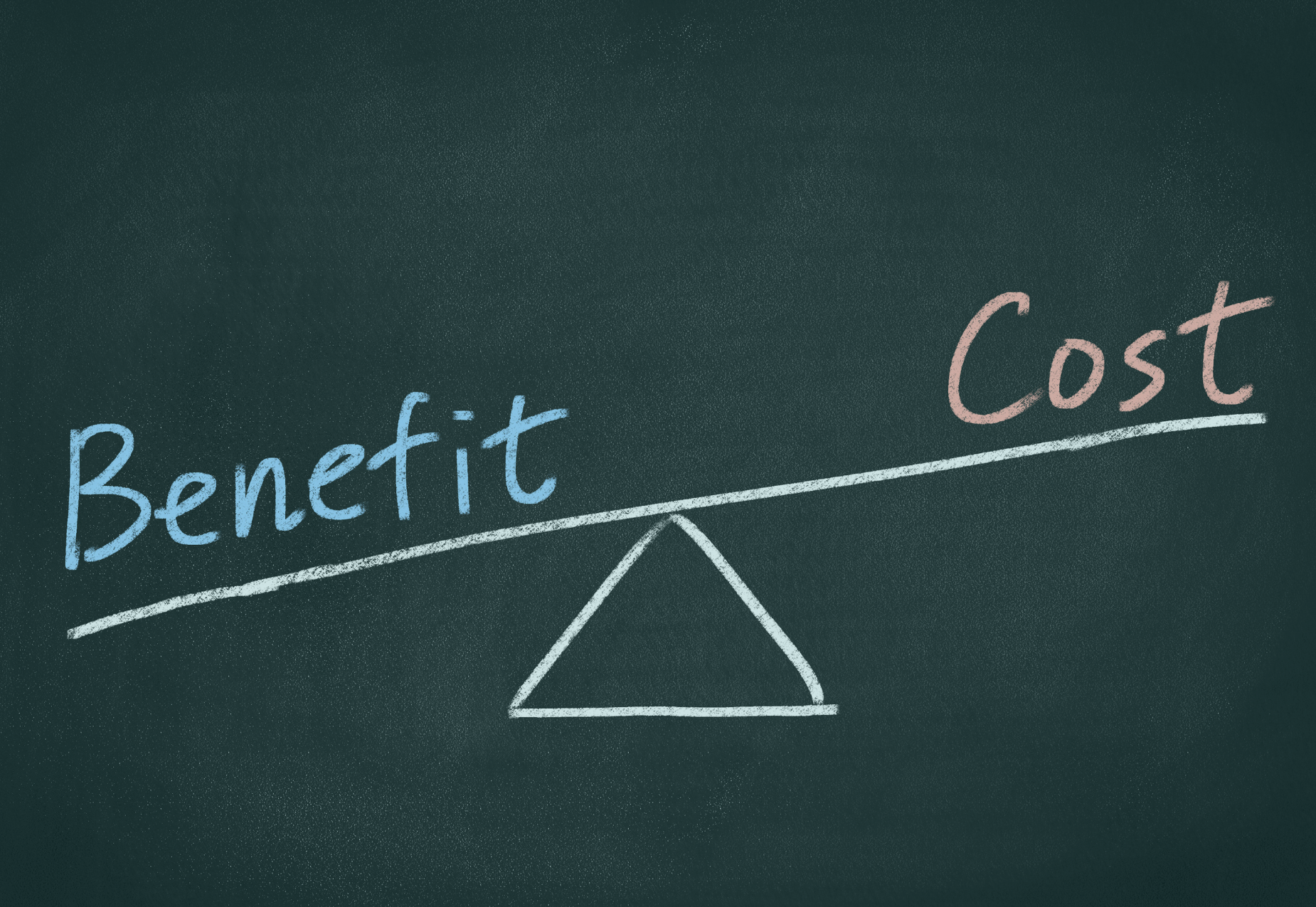

What are the Cost Benefits of Investing in a GRC System?

More and more organisations are currently seeking out technology-enabled GRC…

Are you ready for Consumer Duty?

With eyes firmly on the calendar for the new Consumer Duty Regulations coming…

Has the Motor Finance Industry had its head in the sand?

Ever since the FCA launched a review into Motor Finance and published their…

5 Steps to Improve Your Customer Due Diligence

Last month we looked at third party due diligence and how technology can…

Guide to Operational Resilience

It’s the Monday morning you don’t want. Social media is buzzing because a…

5 Steps To Improve Your Third-Party Due Diligence

All companies use third parties as an essential component in the running of…

Regulation of Buy-Now Pay-Later is Coming

Alice wants a new laptop computer, but it will take her a few months to save…

Funeral Plan Providers – Are You Ready for Regulation Change?

On 29 July 2022, the FCA will start regulating the funeral plans sector. If…

We won! Fintech Awards 2023- 1RS voted Best Risk Management & Compliance Software Solutions

We are thrilled to announce that Wealth & Finance International have…