Counting The Cost (Cost of Compliance Vs Cost of Non-Compliance):

Is your firm spending enough on compliance?

This has been one of the dominant questions over the last few years, and one that is still pertinent to the financial services industry in the post-pandemic world.

In 2021, to keep on top of the volume of regulatory change and to meet increasing regulatory expectations is a big challenge. For many firms, the only option is to throw more people, time, and resources at the problem, the cost of which can soon add up.

The pandemic has introduced new difficulties and now more than ever compliance officers are under pressure to roll out an enhanced compliance programme; whilst under budget pressures, convincing executive management that they need additional resources.

In this article, we explore the growing costs of compliance – and non-compliance – for financial firms.

What do Financial Firms Spend on Maintaining Compliance?

A study revealed that the global spend on financial crime compliance at financial institutions had reached $213.9 billion in 2021 – an increase of nearly 16% on the previous year.

Further research conducted by LexisNexis Risk Solutions also calculated that a total of around £28.7 billion was spent annually in the UK as AML compliance costs. Spending by UK firms on regulatory compliance was expected to continue to rise and exceed £30 billion by 2023, reflecting increasing board-level concerns over reputational risk and higher fines.

A recent global survey suggested that a third of banks spend more than 5% of revenue on compliance. Other research conducted by Thomson Reuters indicated that 62% of their respondents said they expect the cost of time and resource devoted to conduct risk issues to increase in 2021.

Although jaw-dropping, these figures are not static and do not reflect the potential for regulatory acceleration and complexity in the coming years. To succeed in the post-pandemic world, financial institutions need to find a cost-effective approach that enhances their compliance processes, customer experience, and financial capabilities.

What do Financial Firms pay for Non-Compliance?

Financial regulatory authorities have always maintained a strict compliance regime and handed out hefty fines for those who fail to comply. In recent years the pace of these fines shows no signs of slowing down:

- By the summer of 2020, global regulators had already issued $5.6 billion in fines against financial institutions.

- Research in 2020, showed the breakdown in fines for non-compliance was 20% from employee errors, 20% as a result of criminal misconduct, and 60% owing to cyber-attack related fines.

- One of the largest fines handed out by the FCA in 2020 was split between Lloyds Bank plc, Bank of Scotland plc and The Mortgage Business plc. The penalties totalled £64,046,800 and were handed out due to failures concerning the poor handling of mortgage customers in arrears or payment difficulties.

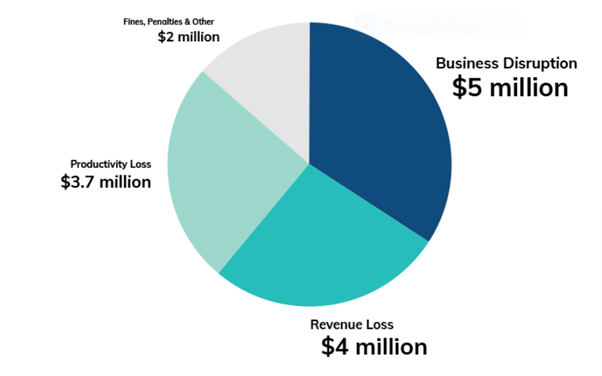

But these fines, once again, are not entirely a true reflection of the actual cost of non-compliance for firms. The average total cost for a data breach in 2020 was reported to be $3.86 million taking an average time of 280 days to identify and contain. When considering the true cost of non-compliance firms must factor in costs of business disruption, revenue, and reputational loss:

Source: Ascent

In fact, a report from Globalscape inferred that the cost of non-compliance was twice the cost of compliance. Fundamentally because non-compliance costs not only include fines and settlements but business disruption, productivity loss, and revenue loss also. Leaving many to question can they afford the risk?

In fact, a report from Globalscape inferred that the cost of non-compliance was twice the cost of compliance. Fundamentally because non-compliance costs not only include fines and settlements but business disruption, productivity loss, and revenue loss also. Leaving many to question can they afford the risk?

Staff Vs Tech

Having shone a spotlight on the price of compliance, the next question concerning compliance costs is staff versus technology and where to invest on a budget…

Each has its advantages and disadvantages. Staffing provides more ‘eyes’ and accountability, however, the increased costs in salary, training and managing more staff is a disadvantage. The advantages of technology include real-time monitoring, centralized workflow processes, increased efficiency and reduced long terms costs. The disadvantages are the initial adaptation and training for the new system.

Ideally, firms should have a good blend of personnel and technology. Technology provides firms with the tools and can enhance compliance programmes, while staffing is critical to review and analyse the results the technology produces.

Under the strain of regulatory burden, firms appear to be spending more time and costs on staffing, a short-term solution. Rather than implementing a technological solution that could bring about longer-term benefits.

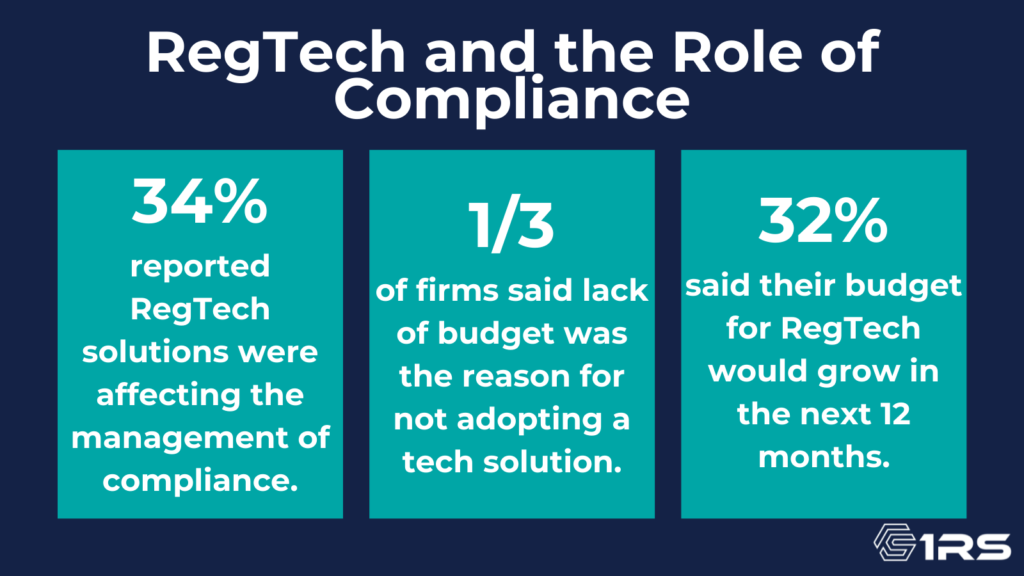

A regulatory intelligence annual survey report Fintech, Regtech and the Role of Compliance for 2021 found that 16% of firms had implemented a RegTech solution, with a further 34% reporting that RegTech solutions were affecting the management of compliance. Other findings from this report include:

- 27% of firms lack a budget for RegTech solutions compared with just 4% of G-SIFIs.

- 32% of firms said their budget for RegTech solutions would grow in the next 12 months while 25% said the budget will stay the same (42% for G-SIFIs).

- The main reason firms had not deployed fintech or RegTech solutions was a lack of investment or budget, cited by a third of firms.

- The greatest benefits of tech solutions reported were an improvement in efficiency, greater transparency in decision-making and cost reductions.

Conclusion

Conclusion

As financial firms prepare for the post-pandemic world and whatever the future might hold, many will be looking to trim costs wherever they can. Nevertheless, as is evident from the findings above, the costs of risk and compliance will be continuing to rise. In order to navigate these tricky waters, financial institutions should consider the right balance of people and technology that will allow them to make the most of their resources.

If you wish to discuss how technology can be a cost-effective solution to managing your compliance going forward, then please contact one of our experts at 1RS.[/vc_column_text][/vc_column][/vc_row]

Blog

5 Ways Technology Can Help with SMCR Compliance

One of the biggest changes to FCA regulation in recent years was the need to…

How To Embrace Technology but Keep Your Humanity – Implementing A RegTech Solution

Today, the majority of our business and personal lives are dominated by our…

What are the Cost Benefits of Investing in a GRC System?

More and more organisations are currently seeking out technology-enabled GRC…

Are you ready for Consumer Duty?

With eyes firmly on the calendar for the new Consumer Duty Regulations coming…

What is CASS and who does it apply to?

If a financial services provider holds or controls client money or assets, then…

Has the Motor Finance Industry had its head in the sand?

Ever since the FCA launched a review into Motor Finance and published their…

5 Steps to Improve Your Customer Due Diligence

Last month we looked at third party due diligence and how technology can…

Guide to Operational Resilience

It’s the Monday morning you don’t want. Social media is buzzing because a…

5 Steps To Improve Your Third-Party Due Diligence

All companies use third parties as an essential component in the running of…

Regulation of Buy-Now Pay-Later is Coming

Alice wants a new laptop computer, but it will take her a few months to save…

We won! Fintech Awards 2023- 1RS voted Best Risk Management & Compliance Software Solutions

We are thrilled to announce that Wealth & Finance International have…